11.1 Consolidated balance sheet

(after profit appropriation)

Fixed assets

(x EUR 1.000)

| Notes | 30-jun-20 | 30-jun-19 | |||

|---|---|---|---|---|---|

| FIXED ASSETS | |||||

| Intangible fixed assets | 1 | ||||

| Research and development costs | 804 | 7.504 | |||

| Goodwill | 124 | 498 | |||

| Concessions, licensces and intellectual property | 1.636 | 2.181 | |||

| 2.564 | 10.183 | ||||

| Tangible fixed assets | 2 | ||||

| Company buildings and land | 13.984 | 14.824 | |||

| Plant and equipment | 6.361 | 6.048 | |||

| Other fixed operating assets | 616 | 643 | |||

| Operating assets under construction | 2.401 | 395 | |||

| 23.362 | 21.910 | ||||

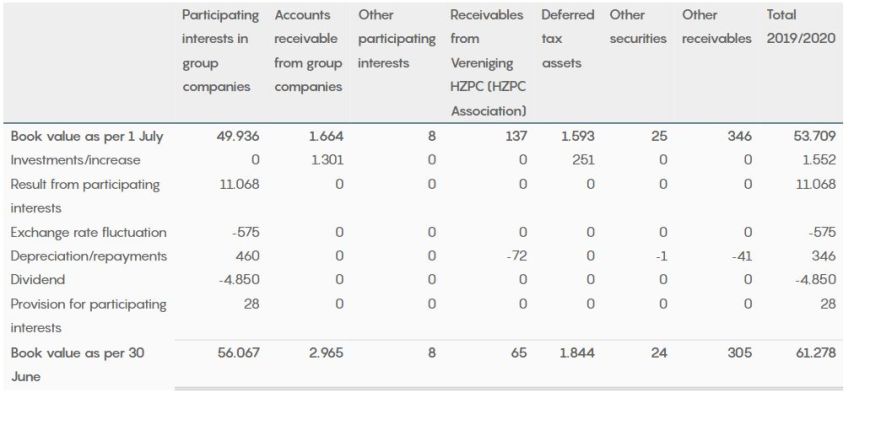

| Financial fixed assets | 3 | ||||

| Participating interests | 1.070 | 1.207 | |||

| Receivables from Association HZPC | 65 | 137 | |||

| Other securities | 25 | 25 | |||

| Deferred taks assets | 2.204 | 1.972 | |||

| Other receivables | 324 | 374 | |||

| 3.688 | 3.715 | ||||

| TOTAL FIXED ASSETS | 29.614 | 35.808 | |||

| CURRENT ASSETS | |||||

| Inventories | 4 | 2.133 | 2.012 | ||

| Trade and other receivables |

|||||

| Trade receivables |

5 | 54.108 | 41.093 | ||

| Accounts receivables from participating interests | 6 | 342 | 189 | ||

| Taxes, contributions and social insurance | 7 | 9.421 | 6.788 | ||

| Other receivables and accrued income | 8 | 15.311 | 13.082 | ||

| 79.182 | 61.152 | ||||

| Cash and cash equivalents | 9 | 33.217 | 30.403 | ||

| TOTAL CURRENT ASSETS | 114.532 | 93.567 | |||

| TOTAL ASSETS | 144.146 | 129.375 |

Liabilities

(x EUR 1.000)

| Notes | 30-jun-20 | 30-jun-19 | |||

|---|---|---|---|---|---|

| LIABILITIES | |||||

| GROUP EQUITY | 10 | ||||

| Shareholders' equity | 53.357 | 53.550 | |||

| Provisions | 11 | ||||

| Pensions | 177 | 164 | |||

| Other provisions | 419 | 423 | |||

| 596 | 587 | ||||

| Current liabilities | |||||

| Debts to credit institutions | 12 | 57.850 | 35.282 | ||

| Accounts payable to suppliers | 14.430 | 16.381 | |||

| Payables to participating interests and companies in which there is a participation | 266 | 300 | |||

| Taxes, contributions and social insurances | 13 | 1.852 | 2.238 | ||

| Dividend to be paid | 784 | 6.074 | |||

| Other debts and accrued liabilities | 14 | 15.011 | 14.963 | ||

| 90.193 | 75.238 | ||||

| TOTAL LIABILITIES | 144.146 | 129.375 |